Does Credit Score Affect Car Insurance Understanding the Impact on Your Premiums

Insurance

|

April 5, 2026

Your credit score can significantly impact your car insurance rates. Insurers frequently utilize credit information when determining premiums, resulting in noticeable variations in costs based on an individual’s credit profile. It’s important to recognize that the credit data insurers use is not the same as the traditional credit score. The latter is a numeric representation of a person's creditworthiness; meanwhile, the former comprises various factors such as payment history, amounts owed, and credit utilization, which play a crucial role in assessing risk.

Your credit score can significantly impact your car insurance rates. Insurers frequently utilize credit information when determining premiums, resulting in noticeable variations in costs based on an individual’s credit profile. It’s important to recognize that the credit data insurers use is not the same as the traditional credit score. The latter is a numeric representation of a person's creditworthiness; meanwhile, the former comprises various factors such as payment history, amounts owed, and credit utilization, which play a crucial role in assessing risk.

The methodology surrounding this practice is not consistent across states, as regulations governing the use of credit information in determining car insurance premiums differ markedly. Some states impose restrictions on the degree to which a credit score can influence premiums, while others permit greater reliance on credit metrics in setting prices. This article will delve into the ongoing debate around the question: does credit score affect car insurance? We will examine how credit scores shape insurance rates, the nuances of state regulations, and provide tips on improving credit to potentially lower premiums.

How Does Credit Score Affect Car Insurance?

When establishing premiums, car insurance companies assess risk through various metrics, among which is the applicant's credit score. Insurers typically assert that individuals with higher credit scores tend to pose lower risks, resulting in fewer claims; consequently, they often offer lower premiums to these drivers. Conversely, a lower credit score can signify higher risk, prompting increased rates.

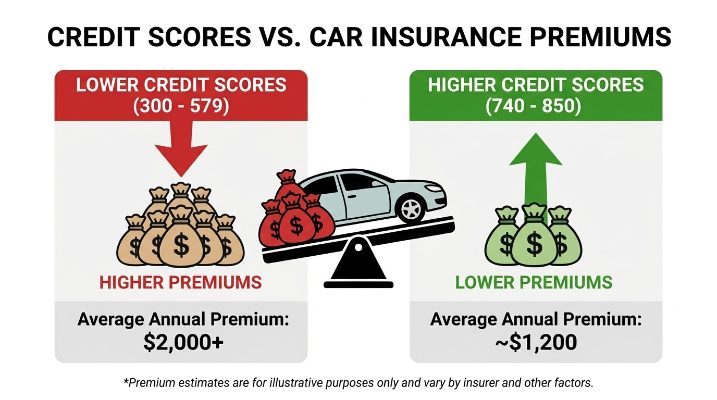

For instance, consider two drivers with identical clean driving records—both having no accidents or violations. If one possesses a credit score of 750 and the other has a score of 600, they will likely encounter a marked difference in their insurance rates. The driver with the higher credit score may enjoy a reduction of around 20% in premiums for the same coverage compared to their counterpart with the lower score. This contrast underscores how responsible credit behavior, such as timely bill payments and judicious credit utilization, directly informs insurance pricing. Ultimately, maintaining a favorable credit score can yield significant savings on car insurance premiums, motivating drivers to manage their credit proactively.

Credit Score vs. Credit-Based Insurance Score

Traditional Credit Score

Traditional credit scores offer a view into an individual’s creditworthiness, reflecting various financial activities such as loans, mortgages, and credit card usage. These scores typically range from 300 to 850, with lower scores indicating a higher financial risk, prompting lenders to utilize them for assessing eligibility for credit products and setting interest rates.

Credit-Based Insurance Score

In contrast, a credit-based insurance score is designed specifically to assess an applicant's credit history within the context of insurance. Insurers leverage this score to gauge risk, as studies have consistently indicated a correlation between credit behaviors and insurance claims. A lower insurance score can lead to higher premiums, mirroring perceived risk, while a higher score can facilitate lower costs.

It is critical to understand that traditional credit scores and credit-based insurance scores serve different purposes, despite both being derived from credit data. One focuses on lending risk, while the other addresses insurance risk. Moreover, not all insurers employ this score in an equivalent manner, with some states placing restrictions on its application. Familiarity with these distinctions allows consumers to manage their credit more effectively, potentially paving the way for lower insurance costs.

Why Do Insurance Companies Use Credit Information?

Insurance companies have long acknowledged the importance of credit information in risk assessment. Risk prediction is foundational in underwriting processes, where insurers scrutinize an individual’s credit history to forecast their likelihood of filing claims. Research corroborates a consistent link between lower credit scores and heightened claim frequency, suggesting that individuals with poor credit present a greater risk to insurers.

Statistical trends reaffirm this rationale, indicating that those with lower credit ratings tend to file claims that are not only more frequent but also of greater magnitude. Such data serves as a predictive tool and shapes premium pricing strategies by segmenting risks according to credit profiles. Insurers categorize policyholders into various risk brackets, imposing elevated premiums on those assessed as more likely to incur claims.

The underwriting process reflects a data-driven approach. Insurers deploy advanced algorithms and historical data to cultivate risk profiles, positioning credit information as a critical factor in their decision-making. Therefore, while understanding that credit scores significantly contribute to underwriting, it's essential to remember that they are among several factors influencing the insurance landscape. Comprehending these processes can empower consumers to manage their credit proactively, appreciating its impact on their insurance premiums.

What Factors in Your Credit History Matter Most?

Several elements within your credit history distinctly affect both your credit score and, consequently, your car insurance rates. Being aware of these components can empower you to make informed financial choices.

Payment History stands out as the most important factor. Consistency in timely payments signals reliability to insurers. For example, just one late payment can adversely affect your credit score and inflate your insurance premiums.

Next is Outstanding Debt. High levels of debt can flag you as a higher risk to insurers, potentially escalating your rates. If you possess maxed-out credit cards or significant loans, this can detrimentally impact your score, highlighting the importance of prudent debt management.

Credit Utilization plays a pivotal role, reflecting the ratio of your credit card balances to your total credit limits; a low utilization rate is desirable. Experts generally recommend keeping this ratio below 30%. For instance, if you have a credit card limit of $10,000 and a balance of $2,000, your utilization of 20% is advantageous.

The Length of Your Credit History also matters. A longer credit history not only bolsters your credit score but also displays stability, demonstrating to insurers a record of responsible credit utilization. A diverse mix of older and newer credit can further enhance this aspect.

Additionally, Recent Credit Applications can influence your insurance score. Frequent credit inquiries may signal potential financial distress, while maintaining fewer applications helps sustain your score.

Lastly, emphasizing Credit Report Accuracy is crucial. Errors on your credit report can lead to unjustifiably high premiums. Regularly reviewing your report allows you to identify and resolve inaccuracies swiftly, thus safeguarding both your credit score and your insurance rates.

In essence, a keen understanding and management of these elements not only help in maintaining a good credit score but also optimize your car insurance premiums, resulting in significant long-term savings.

Common Myths About Credit Scores and Car Insurance

Numerous myths circulate regarding credit scores and car insurance, necessitating clarification of prevalent misunderstandings.

1. Getting Insurance Quotes Hurts Your Credit Score:

Many individuals mistakenly believe that acquiring multiple insurance quotes adversely affects their credit score. However, insurers typically conduct a "soft inquiry," which does not impact your score. Therefore, don’t hesitate to seek quotes.

2. Paying Car Insurance Builds Credit:

Another misconception is that timely payment of car insurance contributes positively to your credit score. While punctual payment of loans can enhance your score, car insurance payments are generally not reported to credit bureaus, thus not affecting your credit history.

3. Bad Credit Means You Can't Get Insurance:

A common belief holds that subpar credit renders one incapable of obtaining car insurance. In reality, while lower credit may lead to higher premiums, it doesn’t disqualify you from securing insurance altogether.

4. Credit Score Is the Only Factor That Affects Rates:

Many individuals assume that a credit score is the sole determinant of car insurance rates. In fact, multiple factors come into play, such as driving history, location, and vehicle type.

5. All States Use Credit Information the Same Way:

Finally, it's essential to recognize that states do not uniformly apply credit information. Regulatory differences exist, with some states imposing restrictions on how credit history influences premium setting.

Understanding these misconceptions is vital for making informed decisions regarding insurance costs and credit management.

Does Credit Score Affect Car Insurance Enough to Matter?

The impact of credit scores on car insurance premiums is profound, with findings indicating that drivers with poor credit can pay as much as 50% more than those blessed with excellent scores. Insurers commonly regard higher credit scores as indicative of lower risk, leading to favorable rates. Thus, it’s crucial for consumers to diligently monitor their credit; improvements in one’s score can yield substantial savings on premiums over time.

When it comes time to explore insurance options, don’t shy away from obtaining multiple quotes. This practice secures the most competitive rates in light of your risk profile. Timing is also paramount; shopping around yearly or following significant changes in credit scores can help nab lucrative deals. Moreover, improving your credit involves maintaining prompt bill payments, reducing debt burdens, and vigilantly checking for errors on your credit report. Striking a balance between these credit improvement initiatives and insurance shopping is central to realizing optimal financial benefits. Taking control of your credit not only influences car insurance costs but also cultivates a responsible stance toward financial management, ultimately leading to empowered decision-making on your finance journey.

Final Thoughts

The relationship between credit information and car insurance premiums is significant and multifaceted. This article outlined how credit scores can fundamentally inform the pricing of car insurance, illustrating the trend that a higher credit score often correlates with lower premium costs. However, it is crucial to appreciate that credit is but one among many elements considered by insurers in pricing policies. Other factors, including driving history and coverage options, are equally vital.

As consumers, proactive management of our financial health becomes essential not only to lower insurance costs but also to enhance overall well-being. By regularly monitoring credit scores and implementing strategies to improve them, considerable savings on premiums can be achieved. Adequate exploration of diverse policies alongside a comprehension of the full spectrum of factors influencing insurance pricing empowers informed decision-making. So, does credit score affect car insurance? The answer is a resounding yes, yet it remains a part of the wider financial landscape.

The overarching takeaway is clear: prioritize sound credit management and insurance understanding to improve your financial landscape. Such measures may lead to better rates and increased confidence on the road.

Was this helpful? Share your thoughts